{kind=link}

Have you ever ever encountered Dave, EarnIn, Brigit, or Chime apps? All these are mortgage software program options. However isn’t it banks that subject loans?

Frankly talking, banks like JPMorgan Chase, Financial institution of America, and Wells Fargo nonetheless have the largest shopper mortgage volumes. Nonetheless, neobanks, digital banks, and different different suppliers are step by step rising their market share.

For instance, the worth of the Brazilian neobank Nubank has moved from $58 million in 2019 to round $3.2 billion in 2023. The market share of purchase now, pay later platforms, reminiscent of Klarna and Afterpay, has additionally risen all around the world.

Furthermore, in 2024, digital banks issued loans amounting to about $13 trillion, which, though 15 instances lower than the quantity offered by conventional banks ($200 trillion), can be quite a bit in absolute phrases.

Taking all this into consideration, it turns into clear that growing and having a mortgage utility generally is a worthwhile endeavor. However methods to construct such a platform to take advantage of out of software program improvement providers?

What Is a Mortgage Cellular Utility and How Does It Work?

A mortgage app is a cell software program resolution that makes the lending and borrowing course of attainable by enabling customers to use for loans, get cash, and watch their monetary obligations.

In easier phrases, these apps carry debtors and lenders collectively, who might be people or monetary establishments, and use refined applied sciences to provoke and ease the applying course of.

Credit score apps sometimes characteristic easy, user-friendly screens and dashboards that enable debtors to use for loans, add paperwork, and obtain approvals or rejections on-line.

When accredited, funds are deposited into the account of the borrower, and reimbursement circumstances are set. Generally, credit score apps additionally present lenders with mortgage monitoring, danger governance, and portfolio administration.

Market Overview of Mortgage Lending Cellular App Improvement

It’s an indisputable fact that society has change into extra consuming. When trying on the credit score house owners in international locations around the globe, it turns into clear that increasingly folks depend on loans to cowl their monetary wants.

In Colombia, this quantity reaches 32%, and within the Dominican Republic 38%. However Norway stays the chief, the place the variety of credit score debtors is 40%. However why do folks search for alternative routes to get loans?

Share of mortgage house owners worldwide, as of January 2025, Statista

Conventional banking methods usually contain prolonged paperwork, bodily transactions, and intensive approval procedures which might be not comparable with the trendy tempo of life.

Cellular lending purposes, in flip, present a significantly better equal, the place a lender can take credit score immediately, in some circumstances even inside minutes.

Plus, they’re usually outfitted with machine studying algorithms that quantify creditworthiness utilizing different information, reminiscent of cell phone utilization, spending patterns, and social media posts. This fashion, a prolonged credit score historical past examine is often not wanted.

As well as, in line with Market Analysis Future, there are a variety of different elements that contribute to the expansion of credit score purposes. These embrace:

- Rising smartphone penetration

- Inexpensive cell app improvement

- Regulatory help for fintech developments

- The development of peer-to-peer (P2P) lending platforms.

- The emergence of microcredit choices

- The adoption of AI, blockchain, and automation

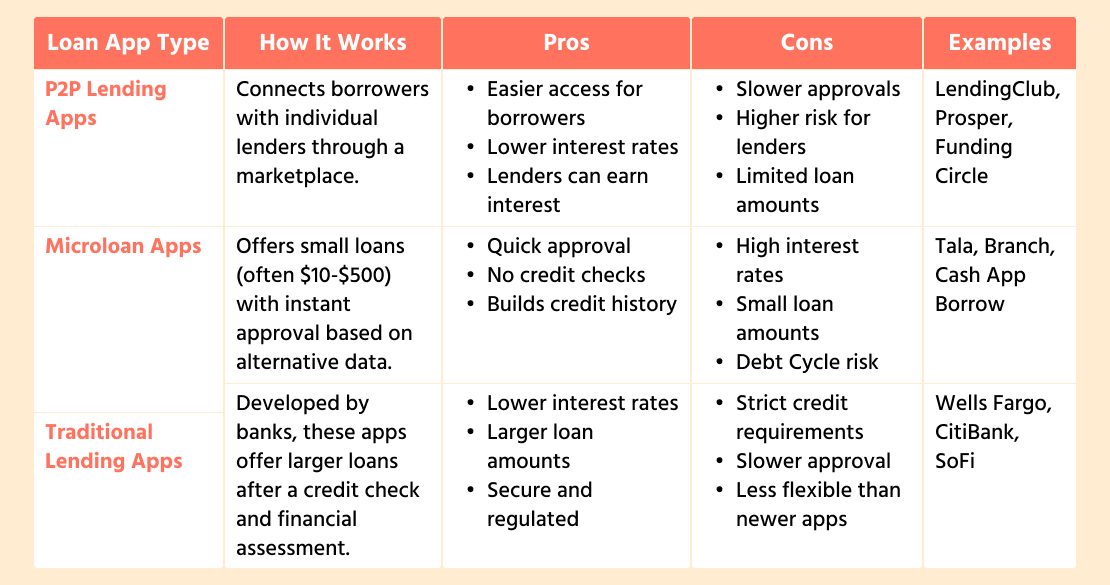

Sorts of Mortgage Options: Peer-to-Peer, Microloan, and Conventional Apps

Not all credit score apps are alike. Some join debtors with particular person lenders, some supply tiny, short-term loans, and a few function similar to old-school banks—however all in your cellphone.

Let’s break down the three major forms of credit score purposes: peer-to-peer (P2P) lending purposes, microloan instruments, and conventional lending platforms—so you realize what differentiates every.

Sorts of Cash Touchdown App Options, Comparative Desk

P2P Lending Apps: Borrow Instantly from Individuals, Not Banks

Peer-to-peer lending instruments function like a market by means of which one particular person borrows cash from one other particular person versus a financial institution or different monetary establishment.

The app acts because the intermediary that connects lenders with debtors, determines the phrases of agreements, and supplies safe transactions.

The way it works:

- Debtors full a type, apply for credit score, and get matched with lenders able to subsidize their requests.

- Lenders select which loans they need to fund, both manually or by means of automated methods that match them with debtors based mostly on danger degree.

- Rates of interest, in flip, are typically set by the platform in line with the borrower’s danger rating.

Common examples: LendingClub, Prosper, Funding Circle

Professionals:

- Simpler entry to loans, even for these with restricted credit score historical past.

- Decrease rates of interest in comparison with conventional loans.

- A good way for personal lenders to earn cash when it comes to curiosity.

Cons:

- Not at all times rapid—approval of the credit score might take a couple of days.

- Better danger to lenders in case the debtors default.

- Credit score quantities could also be smaller than in banks.

Microloan Apps: Small, Quick-Time period Loans for Fundamental Provides

Microloan apps are designed to offer small loans, sometimes for individuals who don’t qualify for normal credit score, reminiscent of folks in rising economies the place penetration of economic merchandise is low.

Microloan options are completely different from P2P platforms as they’re normally secured by a agency or fintech firm moderately than particular person lenders.

The way it works:

- Customers apply for small quantities (usually between $10 and $500), sometimes for short-term use.

- The app employs AI to scan information and resolve if a borrower is eligible.

- When accredited, the credit score is immediately disbursed, and repayments are scheduled routinely.

Common examples: Tala, Department, Money App Borrow

Professionals:

- Very quick approvals—some credit are accredited inside minutes.

- No conventional credit score checks are required.

- Helps folks construct a credit score historical past.

Cons:

- Excessive rates of interest since these are short-term, high-risk loans.

- Debtors can fall right into a debt lure in the event that they don’t plan reimbursement correctly.

- Credit score quantities are restricted, and so they’re not significantly appropriate for giant bills.

Conventional Apps: Banks and Monetary Establishments Go Digital

Banks, credit score unions, or monetary establishments develop conventional platforms to digitalize their mortgage choices. These apps work the identical means as visiting a financial institution to use for a mortgage—solely on-line.

They’re finest for people who find themselves in search of bigger, extra structured loans, reminiscent of private credit, automotive loans, or dwelling mortgages.

The way it works:

- Debtors apply for a mortgage through the app.

- The financial institution opinions their monetary standing, revenue, and credit score historical past.

- After approval, the funds are disbursed and cost preparations are made in common (normally month-to-month) installments.

Common examples: Wells Fargo Private Loans, CitiBank Mortgage Resolution, SoFi

Professionals:

- Bigger mortgage quantities can be found.

- Secure and controlled by monetary authorities.

Cons:

- Stringent necessities—debtors should present a optimistic credit score historical past and proof of revenue.

- It is going to take longer to qualify than microloan or P2P purposes.

- Much less freedom in comparison with fintech mortgage options.

Which Mortgage Resolution Is Proper for Lending Enterprise?

In the event you’re an entrepreneur making a monetary app, what sort you create will depend on whom you need to serve.

If you wish to supply fast, short-term credit to folks with fewer credit score histories, create a microloan app. If you need debtors to borrow from folks as an alternative of banks, a sort is extra applicable.

Nonetheless, in case you are in search of extra substantial financing, like enterprise or private loans, a basic app is unquestionably the best choice.

Key Advantages of Cash Lending App Improvement

There are numerous advantages to creating your personal credit score utility. For instance, having such an app means you could make cash in quite a few methods, other than mortgage curiosity. You’ll be able to take and supply:

- Mortgage charges

- Premium plans

- Late cost charges

- Accomplice offers

- Advertisements contained in the app

The second profit of getting your personal app is you could lower out the intermediary. This implies you don’t should share your earnings with banks or different monetary establishments.

Regardless of when you choose to supply peer-to-peer lending, microloans, or customary financing, making your personal app means you’ll be able to set your phrases, charges of curiosity, and expenses.

The following benefit is you could attain extra folks given the truth that different suppliers are normally open to a wider viewers and might serve those that have been rejected by conventional establishments.

Not like banks, who depend on credit score scores to resolve whether or not to lend to an individual or not, you should use different sources of knowledge to determine if somebody is price lending to.

This offers you the prospect to assist individuals who might not have a recorded credit score historical past however do want entry to cash.

Lastly, whenever you develop your personal utility, you’re fully free to form it in the way in which that’s most sensible for your corporation. Whether or not you deal in private credit, enterprise loans, or providers like Purchase Now, Pay Later (BNPL), you’ll be able to body an app that can be appropriate in your plans and beliefs.

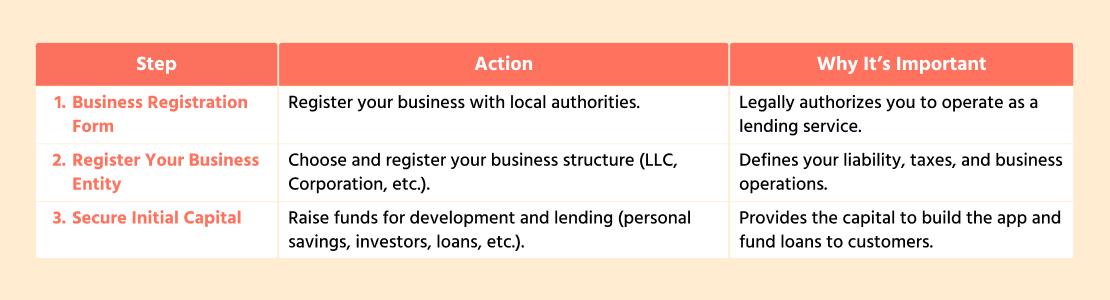

Conditions to Begin Cash Lending App Enterprise

In the event you’re planning to create a cash lending resolution, there are a couple of essential actions you might want to do earlier than you dive into improvement. It’s not all tech—it’s additionally about getting your corporation so as.

Conditions to Contemplate Earlier than Beginning Cash Lending App Enterprise

Fill Out a Enterprise Licensing Kind

Initially, you might want to register your organization. This can take some paperwork along with your state or native authorities in order that they’ll formally document you as a lending service.

Set Up Your Firm

Subsequent, you’ll should resolve what sort of enterprise construction is best for you. Are you going to do it alone, or do you might want to have a staff backing you up? Most companies choose a sole proprietorship, an LLC, or a company, every, nevertheless, with its personal benefits and constraints.

Safe Preliminary Capital

Now, you’ll need to supply some preliminary capital to start out off. Growing an app, sourcing the authorized parts, and operating your corporation prices cash.

The quantity will rely upon how giant your app is and what you need to incorporate. You’ll be able to fund it from private financial savings, borrow from somebody, get a mortgage, and even get traders to fund your idea.

In the event you’re lending cash, you’ll additionally need to ensure you have sufficient funds to lend to your prospects within the first place.

Steps to Create a Cash Lending App

After all, growing purposes from scratch just isn’t straightforward from a technical viewpoint. On the identical time, when you break the entire course of down into smaller components, no less than it’s going to change into clear through which route to maneuver:

1. Preliminary Research and Planning

Earlier than you go forward and create the app, it’s essential to do some planning and analysis. You have to know who your app targets, what different apps supply, and methods to comply with authorized necessities in your space to remain compliant.

On this step, it’s additionally a good suggestion to create a marketing strategy. It is going to enable you to map out how the app will make cash, the way you’ll promote it, and what assets you’ll want.

2. Listing Main Options

Subsequent, you’ll need to ascertain a very powerful components of your utility. Probably the most important are:

- Mortgage utility types

- A option to examine customers’ creditworthiness

- A system for approving loans, automated or/and guide

- A system for cost processing

- Security measures

- A means for customers to trace their repayments

By clarifying these options early on, you’ll know precisely what must be constructed and the way the app will work.

3. Design the Person Interface (UI)

Your app’s UX/UI design actually dictates the way in which folks will work together with it. In case your app is disorienting or troublesome to make use of, folks aren’t going to stay round.

Begin with an easy sign-up course of and make it attainable for customers to use for loans with out frustration. When signed in, customers ought to be capable to see a dashboard the place they’ll see mortgage standing, upcoming funds, and reimbursement historical past.

Be certain that the app is appropriate for telephones in addition to tablets. The design must be crisp, minimal, and user-oriented. So far as colours go, think about blue or inexperienced, that are normally prevalent in finance apps as a result of they confer stability and belief.

3. Select the Proper Expertise

The tech stack has a major function in how the app works and acts. If you’re not a technical specialist and don’t plan to code your self, then no less than it is best to resolve on the next factors.

You’ll want to decide on which OS to attempt for—ought to your app be iOS, Android, or each? With cross-platform frameworks reminiscent of React Native or Flutter, you’ll be able to lower your self a while and deploy for each.

On the backend, you’ll want a dependable cloud service like AWS or Google Cloud. That is the place all of your information can be saved and processed. You’ll additionally want to select a cost gateway, reminiscent of Stripe or PayPal to direct transactions.

For safety functions, you will need to encrypt the person information and use fraud-prevention software program. The safety of the person information ought to at all times be given the best precedence.

5. Develop the App

Now, it’s time to start out constructing the app. Probably the most optimum means right here is to rent a improvement staff that can tackle the frontend (what customers see) and the backend (what’s run within the background) improvement.

They’ll implement all of the options you outlined above, completely take a look at them for bugs, and repair issues upfront to keep away from bigger issues down the road.

6. Add Safety Measures

As a result of your app goes to take care of delicate monetary data, be sure that to encrypt customers’ information so no one else can entry it.

Implement two-factor authentication (2FA) as nicely, which gives an additional safety layer when folks log in, and use fraud detection software program to detect suspicious habits earlier than it turns into an issue.

You additionally must be compliant with trade requirements and rules, together with GDPR (information safety) and PCI DSS (cost card trade information safety customary).

7. Check the App

Earlier than your app sees the world, it’s essential to verify the whole lot works as demanded.

You have to examine that every one options are functioning correctly, from mortgage purposes to reimbursement monitoring, take a look at the app for efficiency, and study safety resilience to catch any vulnerabilities.

By totally testing the app, you’ll show customers have good reception and that the app is secure to make use of.

8. Announce the App

When the software program is prepared, get able to current it to the market. Right here, you’ll must elaborate a advertising program to make it identified.

Double-check that your app’s web page is seen to everybody within the Google Play Retailer or App Retailer and is optimized with the best key phrases so folks can spot it.

9. Watch and Replace

Subsequent, observe the software program’s habits. Be aware how the customers reply to it and see what they recommend. In the event that they determine any flaws or recommend new options, tackle these issues.

Replace your app with a view to dispel any doubt, refine current options, and add new ones. Hold your self conscious of any change in laws and do your utmost to maintain your app legislation-compliant.

Challenges in Mortgage App Improvement and Easy methods to Overcome Them

How exhausting is it to create an app when you by no means handled it earlier than? Frankly talking, like something worthwhile, it comes with its personal hardships. One of many best setbacks is matching all financial directives.

In case your software program product doesn’t adhere to financial standards, you could endure from authorized penalties. To display your progress on this route, you’d higher seek the advice of with a licensed legal professional realizing all of the nuances of economic providers.

Talking of belief, one other main concern is information security. Since mortgage options take care of confidential person data, they change into engaging prey for cybercriminals and scammers.

A breach of knowledge or any criminal activity can severely hurt the fame of your app and even result in huge fines. The safer your app is perceived to be, the extra keen your customers will really feel to share their data.

Subsequent, folks normally are very suspicious of cash apps. In case your app appears to be like under the requirements anticipated or shady, they could avoid it.

One other factor you’ll must pay shut consideration to is the person expertise (UX). The success of any app relies upon largely on how clear and satisfying it’s to make use of. If customers discover it bewildering, perplexing, illogical, or gradual, they’ll shortly substitute you.

To verify this doesn’t occur, design your app to be easy but high-quality. The lending course of must be clearly understood and never topic to misinterpretation.

The following problem you’ll come throughout is credit score scoring and assessing danger. Conventional lending methods depend on credit score scores to fee debtors, however what in the event that they don’t have a credit score historical past?

To unravel this, use different credit score scoring fashions that study customers based mostly on social media exercise, cost historical past, and even behavioral traits just like the frequency of on-time invoice funds.

AI-based credit score scoring software program can even assist fee debtors’ creditworthiness, thereby exposing extra customers to your platform.

Lastly, you could discover it exhausting to retain customers. It’s not sufficient to get customers to obtain your app; you additionally should maintain them concerned and coming again.

Provide them monitoring of the mortgage, reminders for repayments, and customized gives as a form of incentive. Common push notifications and loyalty rewards can even preserve customers in your utility.

But above all, maintain listening to your customers. Their suggestions may help you polish the app and maintain it relevant.

How A lot Does It Price to Construct a Mortgage App?

When making a mortgage app, entrepreneurs usually ask how a lot all that is going to value. The value at all times will depend on many standards, together with how complicated the parts are, whether or not the app goes for one or a number of OS, and whether or not it’s all made in-house or outsourced to a software program improvement firm.

Realizing the approximate bills can help you in higher allocating your finances. Let’s roughly dissect it:

- Information Assortment and Technique Improvement: $5,000–$10,000

- Design and Prototyping: $10,000–$15,000

- Improvement (Frontend and Backend): $50,000–$150,000+

- High quality Assurance: $5,000–$10,000

- Launch, Advertising and marketing, Gross sales: $10,000–$20,000

Within the preliminary design and planning section, you’ll be able to count on to pay for market investigation, wireframing, and pilot testing. This can usually take you from $5,000 to $15,000, relying on the extent of element you need in your analysis and the way a lot work the designers should do.

In the event you’re creating it for each iPhones and Androids, you’ll be on the upper finish of that vary as a result of it’s going to indicate having to assemble duplicate variations for every platform.

The event half, the place coding and backend work is finished, is not any inexpensive. An MVP offering solely the necessities and nothing fancy can be within the spectrum of $30,000 to $50,000.

However you probably have ambitions for high-end options, the associated fee can soar a lot larger—$70,000 to $150,000 or extra.

Additionally it is price mentioning the worth of integrating cost gateways and compliance with financial institution rules, which might be within the vary of $10,000 to $20,000.

Apart from, you’ll must consider lasting expenses for testing, deployment, and maintenance. Testing generally quantities to $5,000-$15,000 once more relying on the complexity.

Deployment expenses lower than the opposite phases, one thing between $1,000 to $5,000. Annual routine updates, gaps and flaws, and safety patches might take you $5,000 to $15,000.

Nonetheless, the upkeep charge can double when you add new options or stumble upon any downside requiring emergency care.

The Function of Authorized Compliance and Encryption

The most important issues you’ve gotten to keep in mind all through the complete improvement course of are authorized compliance and encryption. Why?

Utilizing end-to-end encryption (the place information is rearranged and solely the supposed recipient can unlock it) is important when coping with funds and delicate data. With out sturdy encoding, your customers’ particulars might be in danger, and that might result in main irrevocable safety breaches or harm to the general public picture.

Authorized compliance, by and enormous, demonstrates you comply with the instructions and rules for lending and supervising monetary particulars within the locations the place your app runs.

Totally different areas have completely different legal guidelines about shopper safety, information privateness, and anti-money laundering.

For instance, within the US, you need to obey the Honest Lending Act, and in Europe, the GDPR has strict rules about the way you govern confidential data.

Neglecting these decrees can land you in some severe bother, together with fines, prohibitions, and even license revocation.

The ICO, for instance, has fined British Airways £20m for a consequential information breach that occurred in 2018, ensuing within the licking of non-public information of over 400,000 folks, together with cost data, names, and addresses.

Properly-Identified Examples of Cash Lending Apps to Check with When Making Your Personal App

Whenever you’re growing a lending app, it may be actually useful to have a form of function mannequin you’ll be able to confer with. These lending firms have already tried the waters, so it gained’t be such a nasty concept to encourage or study from them to keep away from the identical errors:

LendingClub

LendingClub is a number one peer-to-peer lending label. It permits debtors to attach with particular person traders who fund their loans. The app gives private loans, enterprise loans, and even auto refinance.

LendingClub’s clear and easy design together with its strong monetary options makes it an excellent template for a peer-to-peer lending app.

Their wonderful document for transparency and favorable mortgage circumstances can yield strong classes in your app, significantly with regard to belief with shoppers and communication.

PaySense

PaySense is a type of money-lending apps focusing on lending private loans to people who might not adhere to the standards for a conventional mortgage.

It lends fast, low-value loans with handy reimbursement schedules. One good factor about PaySense is its ease of use—customers can request loans, get accredited inside minutes, and have funds wired into their accounts.

Money App

Though it began out as a cash switch app, Money App now gives an assortment of economic providers, together with prompt loans and the flexibility to purchase and promote shares and Bitcoin.

Money App is a good instance of methods to make a whole monetary instrument in a single spot. If you wish to implement options like straightforward cash entry or a cell pockets, the Money App is a good prototype.

SoFi

SoFi is one other big within the on-line lending market. It supplies scholar loans, private loans, dwelling loans, and refinancing.

SoFi differs from others in its membership framework, through which debtors obtain entry to premium monetary planning options, profession steering, and even insurance coverage.

All in all, SoFi is a wonderful customary to comply with in establishing a extra profound connection along with your prospects than merely lending.

Kiva

Kiva is a non-profit lending platform that facilities round microloans for people in underserved districts.

It’s really completely different from different lending instruments on the checklist in a means it permits folks to lend small quantities to entrepreneurs and small enterprise house owners in growing international locations.

In the event you think about a extra socially conscious strategy or need to penetrate the peer-to-peer lending market, Kiva supplies an fascinating instance to show to.

Affirm

Affirm is a BNPL utility that permits shoppers to make a purchase and pay for it in components. The appliance is extraordinarily user-oriented, with freedom relating to when and methods to make funds.

In the event you’re going to offer installment-based loans as a part of your utility, Affirm is a good consultant to emulate insofar as making the whole lot easy and simple.

FAQ

- How a lot does it value to create a cash lending app?

By and enormous, mortgage lending app improvement will depend on how a lot you’re keen to spend. For a easy software program instrument with little performance, you’ll most likely make investments between $20,000–$50,000. A sophisticated one with credit score scoring powered by AI, automation, and further security mechanisms ranges from $150,000 and above. Design, platform (iOS, Android, or each), and integrations with third events additionally have an effect on the worth.

- What options ought to a mortgage app have?

No less than, your app ought to embrace person registration, credit score utility processing, credit score scoring, monitoring of repayments, cost integrations, and safety mechanisms. To face out, although, add AI for danger inspection, automated approvals, and buyer care chatbots.

- Do I’ve to stick to any authorized rules to start out a credit score app?

Sure! Mortgage purposes contain cash and private information, so you need to adhere to monetary rules. Within the US, as an illustration, you need to adhere to the Honest Lending Act and California Client Privateness Act. In Europe, you need to abide by GDPR information safety. Overlooking authorized obligations can get your app shut down or fined.

- How do lending apps make cash?

The vast majority of lending purposes make revenues from curiosity on loans, transaction charges, subscription charges, or commissions from collaborations with banks and lenders. Some additionally supply premium options, reminiscent of monetary planning or early entry to loans, for a charge.