{kind=link}

Join each day information updates from CleanTechnica on electronic mail. Or comply with us on Google Information!

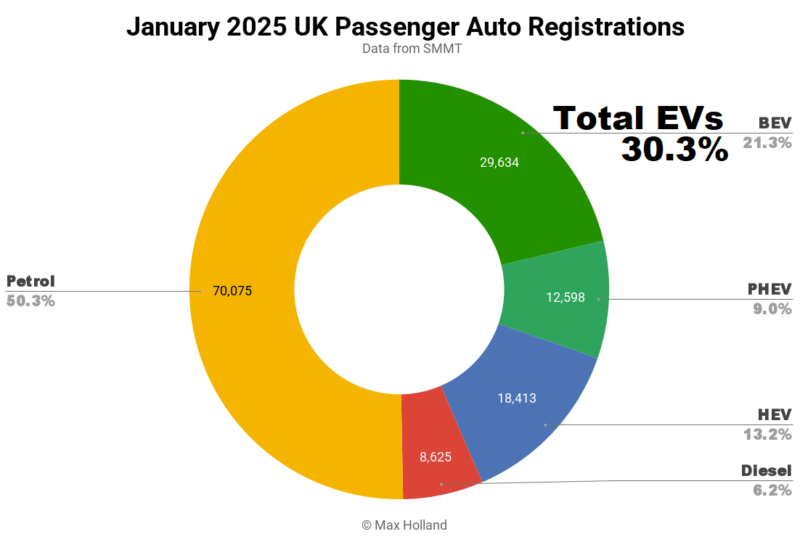

January noticed plugin EVs take 30.3% share of the UK auto market, up from 23.0% year-on-year. BEVs grew quantity by 42% YoY, whereas PHEVs grew 5.5%. Plugin development comes regardless of total auto quantity down 2.5% year-on-year, at 139,345 items. Volkswagen was the main BEV model in January.

January’s gross sales figures noticed mixed plugin EVs take 30.3% share of the UK auto market, with full electrics (BEVs) taking 21.3%, and plugin hybrids (PHEVs) taking 9.0%. These examine with YoY shares of 23.0% mixed, 14.7% BEV, and eight.4% PHEV.

It is a good begin to the yr for BEVs. Recall that the UK began implementing a ZEV mandate in 2024, aimed toward setting steadily rising targets for the proportion of “Zero Emission” automobiles that producers should promote. In actuality this isn’t merely about BEVs – though these play the most important half – however reducing emissions (nonetheless that’s achieved). 2024 set a headline goal of “22% ZEV”, with a small quantity of credit score given for PHEV, and a fraction given for the bottom emission plugless automobiles (e.g. HEVs). In apply, the “22%” translated right into a market-wide 19.6% share for BEVs in 2024, which – together with 8.6% PHEVs and 13.6% HEVs – nearly met the mixture goal.

2025 sees the headline ZEV goal ratchet as much as “28%”. Once more, with some wiggle room it will translate right into a BEV share goal of someplace round 24–25%. This being the case, January’s results of 21.3% is already a great outcome and means that the ZEV mandate “is working”. Regardless of this, unsurprisingly the trade foyer, the SMMT is claiming that producers will “wrestle” to fulfill the goal this yr, and asking for extra carrots for his or her pockets. We are able to ignore most of that.

One legitimate level that the SMMT raises is questioning the logic of making use of a further £410 annual highway tax on BEVs priced above 40,000 – referred to as the “costly automotive complement”. ICE automobiles must pay this, however shouldn’t BEVs get a greater deal (since they nonetheless price greater than their ICE friends)? This additional £410 is because of apply from the beginning of April beneath present plans.

Common readers know that I’m all for extra inexpensive BEVs, however that doesn’t imply that what’s presently a mid-market value household BEV costing £40,995 ought to moderately be taxed an additional £410 per yr greater than a BEV priced at £39,995. Not solely ought to BEVs arguably get a softer contact, however this “cliff” tax method – solely making use of the additional tax, in full, for BEVs priced above £40,000 – appears brainless. The tax charge ought to certainly be proportional (% primarily based) and will slide in, beginning at regardless of the MSRP is in extra of £40,000 (or e.g. beginning at £38,000 or no matter level is smart). That is the kind of calculation that Norway makes use of for VAT tax on “luxurious” BEVs, for instance. Most international locations use a threshold-plus-percentage (and even progressive share) charge for revenue tax, so is that this extra delicate method actually so “laborious to grasp” as is usually claimed?

Simply as an illustrative instance, if the highway tax have been set at 4% for the portion of the MSRP value above £40,000, then the £40,995 automobile would solely pay round £20 per yr in additional tax. Nevertheless a £45,000 would pay £200 additional, and that authentic tax goal (of round ~£400 per yr) would solely be paid by BEVs costing round £50,000. Since this feels roughly the appropriate value level for the place “premium” (or luxurious, should you desire) begins, given the place European BEV pricing is at presently, one thing alongside these strains could be thought of to be truthful. Precise premium / luxurious BEVs costing £60,000+ would pay round £800+ per yr (although that is nonetheless lower than related ICE automobiles that could be paying £1100 to 1500 per yr or extra). The thresholds and % may very well be tweaked over time if mandatory.

If one needed to be fairer nonetheless, since that is ostensibly a “highway tax” used for highway prices and upkeep, why not have a tax which progresses by automobile weight? Once more this tax might begin above a sure threshold, to incentivize automobiles that are as mild as is realistically possible for a easy economic system automotive. With as we speak’s security buildings, automobile weight begins at round 1,000 kg to 1,100 kg (for instance, the Dacia Sandero, the Toyota Yaris, or the Dacia Spring BEV). Then give a further “weight allowance” to BEVs, since batteries and energy electronics are nonetheless pretty heavy at this stage of the BEV expertise curve. Please talk about within the feedback if a sliding weight-based tax (maybe supplemented by annual mileage pushed) could be a fairer solution to pay for roads.

Again to January’s market shares, combustion-only powertrains have been each down in quantity YoY. Petrol-only quantity was down 14.4% to 70,035 items, and diesel-only was down 7.7% to eight,625 items.

Finest-Promoting BEV Manufacturers

In accordance with UK automobile licensing information (the DVLA through EU EVs), the Volkswagen model had the lead within the UK’s BEV market in January, with 8.2% share, simply forward of BMW (8.0%), and Mercedes (7.1%).

The UK’s long-term main BEV model, Tesla, was again in sixth spot in January with somewhat over 5.1% of the market, after certainly one of its greatest ever pushes in December 2024 (20.9% of the market).

As I’ve talked about elsewhere, there’s a story being circulated round European (together with UK) mainstream media that Tesla gross sales are “crashing due to Musk”. No matter one could consider Musk, there’s nicely over 100,000 different individuals working at Tesla. Cool-headed evaluation of the auto market and the traditional sample of gross sales is often absent in such narratives, and the notion of “Tesla gross sales crashing” within the UK (e.g. this mainstream account) leaves out a lot of the important thing context. It leaves out Tesla’s big December BEV share within the UK, Tesla’s ordinary quarterly unevenness, and that many potential consumers are ready for the brand new Mannequin Y to reach (in Could, within the case of the UK’s RHD market).

It’s true that Tesla’s two best-selling fashions now have way more competitors than just a few years in the past, together with from decently competent, albeit easier automobiles, at lower cost factors. The Tesla model’s market share (and quantity) could certainly see one other dip in full yr 2025 in Europe as a complete (following 2024’s dip versus 2023), however the Mannequin Y will virtually definitely be Europe’s best-selling BEV mannequin once more. In any case, it had near 3x the amount of the very best non-Tesla in 2024, as Jose has not too long ago reported with laborious information.

Recall that after January 2024’s UK outcomes, when a few of our CT group have been ignoring Tesla’s ordinary quarterly sample, ignoring the anticipate the refreshed Mannequin 3, and boldly forecasting that the BMW model would overtake Tesla within the UK in 2024? How did that work out? Not nice. Sure, the lead of the Mannequin Y will steadily shrink over time, however don’t count on it to be outcompeted this yr (except Tesla disrupts itself with a less expensive mannequin). After all, right here we’re speaking about manufacturers. When it comes to combining all manufacturers beneath their respective manufacturing group, Volkswagen Group has the lead within the UK, in addition to in Europe.

Within the January model rankings, Peugeot (5.8%) stepped up from 2024’s common share (4.7%), as did Kia (5.6% from 2024’s 3.9%). In the meantime, past Tesla, MG (2.9%) additionally misplaced share in January in comparison with 2024 (5.5%), however nobody is severely arguing that “MG is crashing”. As a result of UK’s right-hand drive system, manufacturing and delivery is usually in batches, so month-to-month variability like that is fairly regular.

Past this month-to-month variability, there are some hints at strikes by new fashions, although our information for that is at all times patchy, sadly. The Kia EV3 appears to have had its finest month but, with round 900 items in January. The Ford Explorer additionally had an honest month with round 650 items (although down from its December meet-the-ZEV-target push). The Dacia Spring maintained an honest quantity of round 350 items. On the premium finish, the brand new Volvo EX90 continued to ramp up, to round 60 items, and the brand new Audi S6 e-tron noticed round 140 items (together with RS6 variants).

Let’s verify in on the 3-month rankings:

Given what we mentioned above about quarterly patterns and the extra month-to-month variability within the UK RHD market, this chart provides a greater image of the bottom actuality (although even right here, the late 2024 push to fulfill the ZEV mandate distorts issues – see the 2024 full yr rating for an extended common).

Right here, the highest 5 manufacturers are all the identical ones as in full yr 2024, although barely reshuffled and with an additional push (notably in December) having come from Volkswagen to fulfill the ZEV mandate deadline. Mini is increased than its common, once more due to an enormous December push, and that’s much more the case for Ford. Many of the others aren’t too far off their long run averages, however once more – verify that 2024 rating for extra context.

When now we have the complete Q1 information, and may examine it to the 2024 This fall information, we can see extra clearly which manufacturers have been within the greatest rush to fulfill the 2024 ZEV mandate.

Outlook

January’s 2.5% YoY drop in auto market quantity is inside regular variation. The broader UK economic system is simply lukewarm, although higher than some neighbours, with newest Q3 2024 GDP information displaying 0.9% YoY development, and This fall’s outcome presently anticipated to be 1.0%. Inflation shaved to 2.5% in December (newest), and rates of interest have simply lowered from 4.75% to 4.5% over the previous week or so. Manufacturing PMI remained destructive in January, at 48.3 factors, although was up from December’s 47.0 factors.

The ZEV mandate launched in 2024, amidst a lot grumbling from intransigent legacy auto, did ultimately lead to an honest bump in BEV share, and accelerated the transition in comparison with many neighbouring European international locations. With 2025’s tightening mandate, now we have to guess that it’s going to even be efficient once more this yr, and little question amidst much more grumbling.

What are your ideas on the UK transition to EVs? Are you planning to get an EV in 2025 or are you continue to ready for “future” specs? Please leap into the dialogue under to share your perspective.

Chip in just a few {dollars} a month to assist assist impartial cleantech protection that helps to speed up the cleantech revolution!

Have a tip for CleanTechnica? Wish to promote? Wish to counsel a visitor for our CleanTech Discuss podcast? Contact us right here.

Join our each day publication for 15 new cleantech tales a day. Or join our weekly one if each day is simply too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage